Local shop owners say bill would hurt consumers while lining insurance companies' pockets

This item is available in full to subscribers.

To continue reading, you will need to either log in to your subscriber account, or purchase a new subscription.

If you are a current print subscriber, you can set up a free website account and connect your subscription to it by clicking here.

If you are a digital subscriber with an active, online-only subscription then you already have an account here. Just reset your password if you've not yet logged in to your account on this new site.

Otherwise, click here to view your options for subscribing.

Please log in to continue |

EVANSTON — A bill that local body shop owners said would hurt consumers and “impact every [auto] repairer in the state,” is making its way through the Wyoming Legislature. After passing committee 5-0, and clearing the full Senate with a 20-10 vote, Senate File 95, “Aftermarket parts,” is in the House, waiting to be introduced.

Currently, insurance companies are required to cover original equipment manufacturer (OEM) parts or aftermarket parts, which are not built by the original vehicle’s manufacturer. SF 95 would allow insurance companies to cover only the cost of aftermarket parts. Should the consumer insist on original manufacturer parts, insurance companies could shift the extra cost for OEM parts to the consumer. The parts included in the bill are limited to “sheet metal, plastic, composite, fiberglass or carbon fiber parts that generally constitute the exterior of a motor vehicle.” It would include both inner and outer panels. The bill also specifies that the parts would have to be of “like kind and quality.”

Still, local body shop owners told the Herald the bill, which is co-sponsored by Sen. Wendy Schuler, R-Evanston, is a terrible idea for body shops and consumers alike, and it compromises safety while lining the pockets of insurance companies.

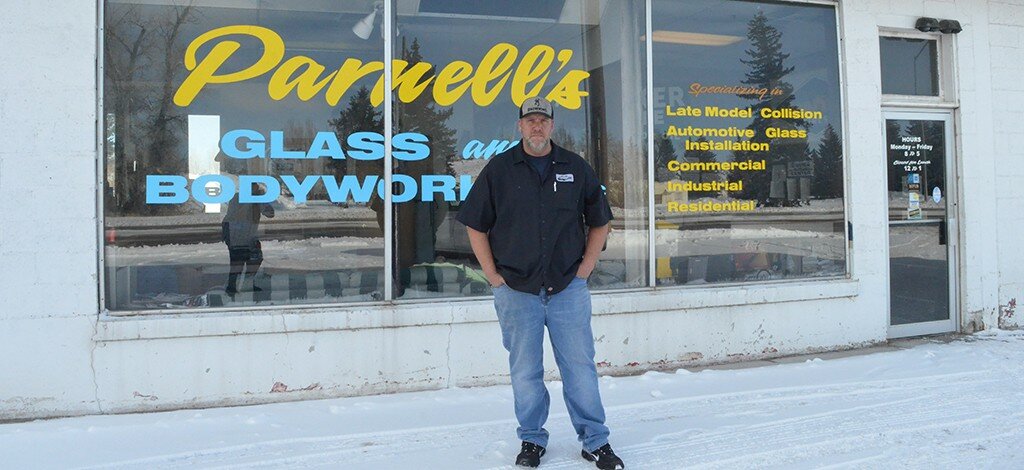

“All [like kind and quality] means is it’s supposed to fit whatever make, model, car, year — it doesn’t have anything to do with crash rating,” Parnell Lym, owner of Parnell’s Glass & Body Works, told the Herald. “It’s their way of getting around the red tape of not having to meet those regulations. They don’t test any of that.”

Lym said that without crash ratings, there’s no way to tell what a collision could do to an aftermarket part that’s hit by another vehicle, and there’s no way to determine whether that would increase the danger or likelihood of injuring a vehicle’s occupants.

If SF 95 becomes law, Lym said, “We’re going to be using sub-par materials to repair people’s cars to get them back to ‘pre-accident condition’ — and that would be impossible.”

Another local body shop owner, Matt Rex, of T Bar S Body Shop in Evanston, agreed with Lym.

“They (aftermarket parts) don’t ever fit right, they’re not molded correctly. … The only way aftermarkets make parts is by buying the original and reverse engineering it or waiting until the patent expires and using old, outdated molds,” Rex said.

Primary bill sponsor, Sen. Tara Nethercott, R-Cheyenne, said she’s fine with the regulations currently in place.

“The regulation of the aftermarket parts industry is sound,” she told the Herald.

Nethercott directed the Herald to SEMA.com, the official website for the Specialty Equipment Market Association. There, SEMA provides a brochure that explains how the National Highway Traffic Safety Administration regulates automobiles and auto parts at the federal level.

But according to the brochure, “… NHTSA has no authority to ‘approve’ or ‘disapprove’ vehicle equipment. The equipment is self-certified.”

Lym and others said the legislation would lead to many voided warranties, hurting consumers.

“The biggest thing for people like me is going to be warranty issues down the road,” Lym said.

Nethercott disputes that and said, “The FTC-Consumer Protection Division clearly states that the use of aftermarket parts does not void a warranty.”

But there are clauses in the Federal Trade Commission regulation to which Nethercott referred. And that’s one concern of the Wyoming Department of Insurance, which opposes SF 95.

Wyoming Deputy Insurance Commissioner Jeff Rude explained it this way: “If I buy a new Ford pickup, Ford cannot mandate that I use Ford parts. … But when I don’t, if the part is defective or installed incorrectly and the parts damage other parts of the vehicle, Ford will void the entire warranty.”

He said the department is opposed to the bill because “we think that it does away with consumer protection that’s been on the books since the late 1980s.”

Lym said shops like his couldn’t stand by the aftermarket parts, either.

“If they make us use those types of parts, we can’t stand behind them,” he said. “They can’t prove that they’re equal or better than the OEM parts we’re using now.”

Rex said it should be up to insurance companies to get their customers’ vehicles in pre-accident condition.

“Aftermarket parts are for someone who doesn’t have insurance, just trying to get their car on the road, trying to save money,” Rex said. “If you buy a 2019 Chevy and get into a wreck, you’ve insured that truck and those parts as a 2019 Chevy. Would you want some aftermarket part, or would you want your 2019 Chevy parts?”

The Automotive Service Association (ASA) is also opposed to the legislation.

The ASA did not return a request for comment by press time; however, according to searchautoparts.com, which follows automotive legislation nationwide, ASA’s Washington, D.C. representative Bob Redding said of SF 95: “This is legislation that has been tried with little success over the years. What state agency is equipped to evaluate the certification standard of aftermarket crash parts? Who will certify? How does this protect consumers? And the National Highway Traffic and Safety Administration (NHTSA) has rebuked any effort to develop certification for aftermarket parts or standards.”

SF 95 would require aftermarket parts to be sufficiently and permanently labeled by their manufacturer. And it would require that aftermarket parts be certified by a nationally-certified organization, though the bill does not specify the organization. It would also require repairers to disclose to the consumer when aftermarket parts are used.

Schuler was one of 19 senators to approve SF 95. She did not return multiple requests for comment by press time.

Neither of Uinta County’s representatives in the House currently support the bill.

Rep. Danny Eyre, R-Lyman, said consumers have voiced their opposition to SF 95. “I have received a lot of feedback indicating that policy holders do not want to risk having a second-rate repair job done by the use of aftermarket parts,” Eyre said. “The repair shops are also opposed to the bill. So, right now I am opposed to the bill. Unless someone can show how to guarantee that the aftermarket parts actually are equal or greater in quality to the OEM parts, then I will remain opposed.”

Rep. Garry Piiparinen, R-Evanston, said, “I have always liked ‘genuine GM parts’ (as I heard growing up in Detroit). Generic parts have always worried me. Costs probably would be lower, but I need to hear more of the testimony when it comes to the House.”

Nethercott said insurance companies are tightly regulated by the Wyoming Department of Insurance.

“In very generic terms,” Nethercott said, “the price of insurance is made up of expected losses, expenses and profit. Typically, the profit rates stays (sic) the same no matter the losses and expenses. Thus, if there is a saving on losses (i.e., paying claim) that will place downward pressure on rates. The bottom line is, insurers pass on savings to. . . [consumers] through rates.”

Both Lym and Rex, two of the body shop owners in Evanston, were leery, to say the least, of that claim.

“It’s insanity,” Lym said, “because the consumer is going to continue to pay the same premium, but the insurance company’s only going to increase their bottom line.”

Rex also said the idea of insurance companies passing on the savings is BS.

“It’s a scapegoat for the insurance companies trying to make more money,” Rex said. “When was the last time an insurance company said, ‘Hey, we made too much money, we’re going to lower your rates?’ They never lower your rates. That is a bogus line from the insurance companies trying to get this bill to pass. They never pass anything on to the consumer other than raising your rates. I’m 42 years old and I’ve had insurance since I was 17. I’ve never seen insurance rates go down.”